Confidence in German Economy Plunges as GDP Contracts

German GDP fell by 0.1% in Q2 as 'economic crisis' becomes 'increasingly entrenched'

Investor confidence in Germany experienced its steepest decline in about two years as Europe’s largest economy contracted on slowing exports, geopolitical concerns, and faltering investments, according to the Zew Institute.

The ZEW Economic Sentiment index, an expectations’ gauge, plummeted to 19.2 in August, its lowest level since January, and down 22.6 points below the previous month, the non-profit German institute said on August 13. The last time sentiment fell as steeply was in July 2022, it said.

“The economic outlook for Germany is breaking down,” Zew President Achim Wambach said. “It is likely that economic expectations are still affected by high uncertainty, which is driven by ambiguous monetary policy, disappointing business data from the US economy and growing concerns over an escalation of the conflict in the Middle East.”

The drop in investor confidence was much lower than the 34-level forecast in a Bloomberg survey. An index of current conditions also declined more than expected.

GDP Contraction

The results of the Zew index were announced after the Federal Statistics Office, Destatis, released data on July 30 showing the country's gross domestic product (GDP) fell by 0.1% in the second quarter compared to the first quarter. The contraction matched analysts' estimates surveyed by FactSet.

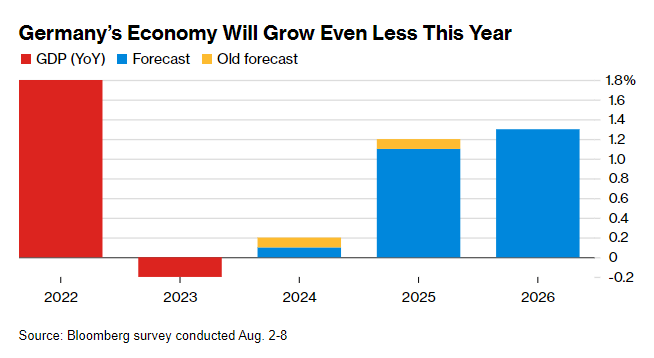

Germany’s GDP is expected to rise 0.1% in 2024, down from a prior forecast of 0.2%, according to a Bloomberg survey, and a 0.2% GDP contraction in 2023. Analysts also trimmed their outlook for 2025 by 0.1% to 1.1%.

This mediocre forecast underscores the difficulties facing Chancellor Olaf Scholz’s government, which has struggled to achieve consistent economic growth since taking office. Germany’s economic struggles are compounded by long-standing structural issues that have eroded its competitiveness.

Manufacturing, traditionally a pillar of Germany's economic strength, has been particularly hard-hit. While factory orders and industrial production improved in June 2024, this uptick has not been enough to compensate for the overall decline in output. Exports, a key driver of Germany’s economy, declined by 1.6% to €801.7 billion in the first half of 2024, highlighting the ongoing struggles in the manufacturing sector.

“The economic crisis is becoming increasingly entrenched at a level of stagnation that frustrates everyone,” Minister for Economic Affairs Robert Habeck said on August 13. “The measures that have been taken so far aren’t sufficient to overcome the high interest rates, the lack of demand from abroad, but also the structural problems that we have in Germany.”

Global Factors

Global factors are also hurting Germany’s economic prospects. Expectations for the eurozone, the US, and China have also deteriorated “markedly,” which “expressed itself in a turmoil on international stock markets,” ZEW's Wambach said.

Stocks on Wall Street tumbled sharply on August 5 amid growing fears of a slowing US economy that set off another sell-off for financial markets worldwide. The DAX declined by 1.82% on August 5, ending the session at 17,339, and is down 1.9% during the three-month period ending August 16.

“The German government said that the weakness was due to a drop in business investment in equipment and structures,” Deloitte Insights wrote on August 13. “Investment in Germany has been hurt by several factors including relatively high energy costs, weak demand in China, weak domestic demand, and intense competition from China and the United States.”

A direct military conflict between Iran and Israel may erode the marginal economic growth that the 27-member European Union (EU) has recorded this year if a steep rise in energy and shipping prices disrupts global trade. The World Bank predicted in April that oil prices could climb above $100 a barrel if there were severe disruptions in oil supplies from the Middle East.

Positive Developments

While the outlook is negative, there have been positive developments for the German economy.

Germany’s inflation, which peaked at 11.6% in October 2022, stood at +2.3% in July 2024, according to a Federal Statistical Office report on August 9. The prices of energy products in July 2024 declined by 1.7% year on year, while the prices of household energy (-3.6%) were down in July 2024 from a year earlier.

German industrial production rose by 1.4% in June compared to the previous month, according to the Federal Statistics Office, above estimates of 1.0% rise analysts polled by Reuters expected. However, it was down an annual 4.1% for the month.

“The positive development of production in industry in June 2024 was mainly attributable to the increase observed in the automotive industry (+7.5% on the previous month after seasonal and calendar adjustment), following a 9.9% decline of production in this branch in May 2024, the Federal Statistical Office said on August 7.

Despite the positive production figures, the German automotive industry faces challenges such as order shortages, supply chain disruptions and increased capital expenditures for companies transitioning to electric vehicles. However, car registrations in Germany increased 5.4% in the first half of 2024 and 6.1% in June, driven by increase registrations in petrol and hybrid electric (HEV) cars.

BMW

BMW (BMW.DE) delivered nearly 600,000 vehicles in 2024, contributing to an overall EBT margin of 11.4%, with automotive EBIT margin hitting 8.8%, with declines in China offset by strong sales in Europe and the US. In its earnings call on August 1, BMW maintained an EBIT target within the range of 8% to 10% and a ROCE of 15% to 20% despite rising manufacturing costs.

The solid financial results of BMW were partially supported by EV sales surging by 27.9% and HEV cars increasing in Germany by 24.7%, pushing the market share up to 29.5% in June compared to 2023, which can be attributed to BMW’s flexible production lines which can accommodate combustion, hybrid and hydrogen-powered cars.

BMW trades at a PE ratio of 4.9, which is below the 3-year industry average of 5.6, positioning the company as a strong candidate for growth as analysts have set a fair value of 109 EUR of its stock, presenting an upside of over 30%.