Dovish ECB Drives 7% EURUSD Drop in Q4

Political instability in France and Germany poses significant risks to the eurozone recovery

The euro fell by around 7% to 1.035 against the US dollar (EUR/USD) in the fourth quarter of 2024 on the heels of a dovish European Central Bank (ECB). The bank reduced its benchmark interest rate for the fourth time in December amid cooling inflation and lackluster growth.

The final 25-basis-point interest rate cut of the year has left a dovish ECB a cumulative 100 basis points lower since commencing its easing cycle in June last year.

"The disinflation process is well on track," ECB President Christine Lagarde said during a December 12 press conference. With inflation expected to decline to 2%, the central bank dropped its commitment to keep rates "sufficiently restrictive," signaling a more dovish stance ahead.

Even hawk ECB policymaker Isabel Schnabel noted at an event in Paris on December 16 that while "risks and uncertainties [remain], lowering policy rates gradually towards a neutral level is the most appropriate course of action." Lagarde and Schabel disagree on where neutral sits, with the ECB defining it in the 1.75%-2.5% range and Schnabel seeing it at 2%-3%.

While markets expect Europe’s central bank to cut a full percentage point to a neutral 2% in 2025, Goldman Sachs’ Sven Jari Stehn expects a more dovish ECB to cut rates to 1.75% due to trade policy uncertainty and go as low as 1.50% should the region’s economic outlook worsen.

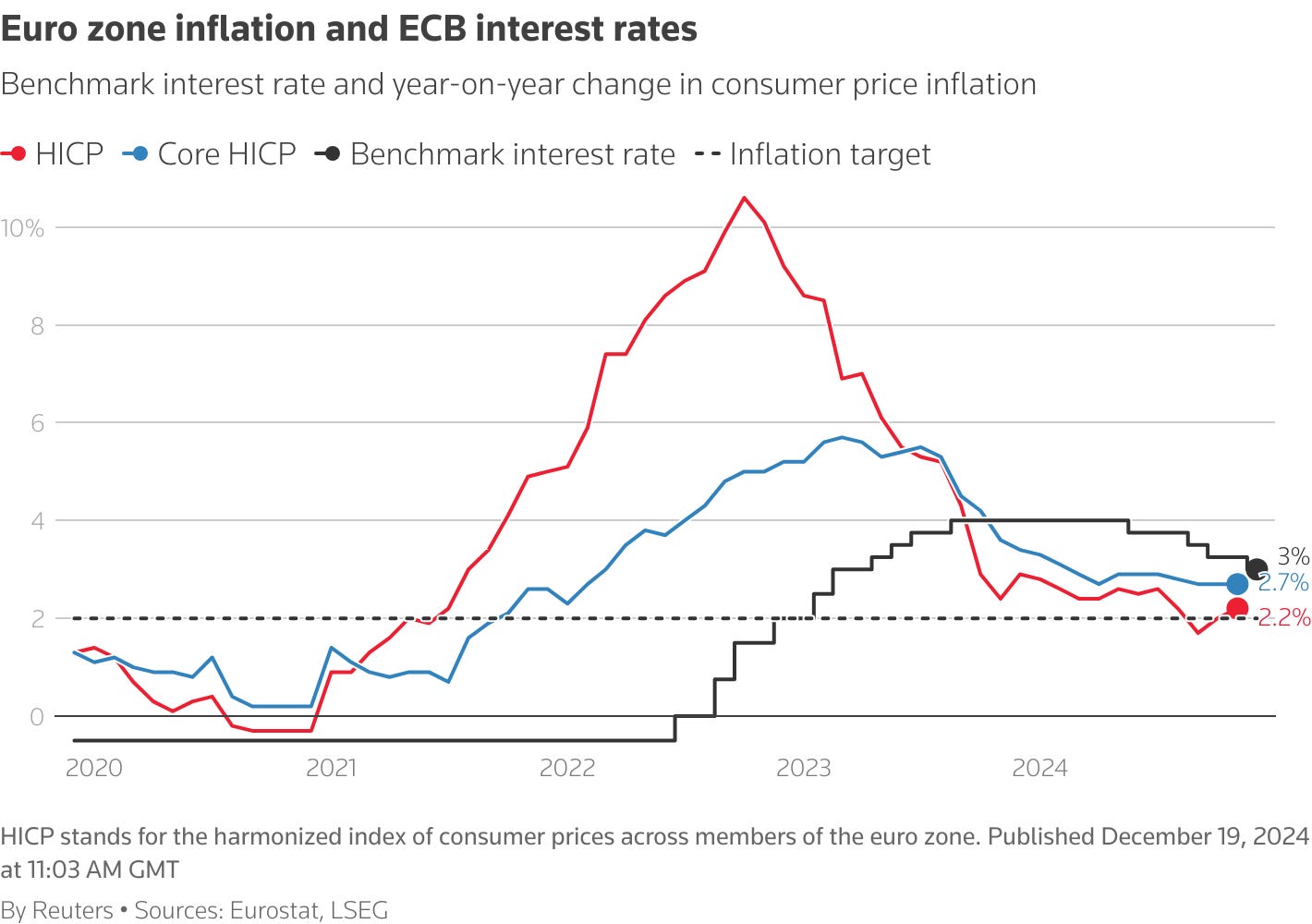

Falling Eurozone Inflation Supports Dovish ECB

Ahead of the ECB’s first interest rate cut in Q2, Eurozone inflation fell to 2.5% year-on-year (YOY) from 5.5% in June 2023 and the peak of 10.6% in October 2022, according to Eurostat data.

The decline follows falling electricity and gas prices, easing supply chain pressures, and the lagged effects of previous monetary tightening.

December staff projections forecast headline HICP will stabilize at 2.1% in 2025, with core inflation sliding to 2.3% from 2.9% in 2024. Before the meeting, staff had projected in July, similar to June’s projections, that headline inflation would be slightly higher at 2.2% in 2024.

Notably, ECB Vice President Luis de Guindos acknowledged in November that "concerns about high inflation have shifted to economic growth," warning of a trade war scenario “extremely detrimental to the world economy.”

Eurozone inflation rose above the bank’s target of 2% in December to 2.4% from 2.2% in November, matching expectations. However, this is unlikely to change the course of a dovish ECB, despite record-low unemployment figures on Tuesday adding pressure on prices.

Out of the Eurozone’s powerhouses, France is an outlier in joblessness amid the economic and political challenges it faces.

Political Instability Adds Extra Layer of Complexity

As France continued to face political instability, President Emmanuel Macron became involved in controversy after accusing Elon Musk of election interference on Monday.

“Who could have imagined, 10 years ago, that the owner of one of the world’s largest social networks would intervene directly in elections, including in Germany?” Macron said.

France lacks a functioning government until the June 2025 elections as Marcon reappointed his fourth prime minister to pass a budget and avoid a looming financial crisis following the resignation of Prime Minister Michel Barnier.

Despite France’s Macron not mentioning Musk by name, Germany’s vice-chancellor, Robert Habeck, said on Monday that the billionaire looks to weaken Europe in a bid to avoid social media regulation.

Musk posted on X on November 8 last year that Olaf Scholz, Germany’s Chancellor, is a “fool,” sparking criticism. This follows the coalition’s collapse on the heels of a lost vote of confidence, with the country now facing snap elections in February.

France and Germany Weigh on ECB Growth Outlook

Political instability in France and Germany poses significant risks to the eurozone recovery after two of the most powerful governments in the EU collapsed. This could result in more dovish ECB easing as risks continue to weigh on the region’s financial stability.

"A significant number of corporate insolvencies are likely next year," Germany’s Bundesbank said. "Default risk for non-financial corporations is likely to remain elevated in 2025 given ongoing structural change and the continued economic weakness," it said.

The OECD expects GDP growth in France to deteriorate to 0.9% in 2025 from 1.1% in 2024 and just a 0.7% growth in Germany in 2025 from stagnating in 2024. Germany represents around 30% of the region’s GDP.

“I’m not overly surprised to see France’s central bank governor has become one of the most dovish members of the ECB governing council,” senior HSBC economist Fabio Balboni told the Guardian.

Trump Tariffs Could Support Dovish ECB

The lack of leadership in Paris and Berlin leaves European Commission head Ursula von der Leyen and Polish and Italian prime ministers Donald Tusk and Giorgia Meloni or Hungary’s Viktor Orban with the challenging task of negotiating US-EU trade relations.

President-elect Donald Trump warned the EU in late December of a “tremendous deficit with the United States,” urging the region to “make [it] up … by the large-scale purchase of [...] oil and gas.” Trump campaigned leading to the November 5 elections for global tariffs of 10%-20% on all imports to the US.

In the days following the US election, von der Leyen said that the region could rump up its liquefied natural gas (LNG) imports to avoid a repeat of 2018. “Why not replace [Russian gas] by American LNG, von der Leyen said, just weeks before a 5-year contract supplying Russian gas to Europe via Ukraine ended.

While Europe grapples with geopolitical uncertainty stemming from the Middle East, potential inflation pressure adds complexity to a Eurozone’s outlook and a dovish ECB.

Eurozone Growth Outlook Remains Fragile

Eurozone GDP growth declined to 0.5% in Q2 2024, compared to 0.6% in Q2 a year ago and 4.1% in Q2 2022.

Dovish ECB staff projections following the December meeting point to a modest 0.7% GDP expansion in 2024 and 1.1% growth in 2025. In September, staff expected growth of 0.9% and 1.4% from 0.8% and 1.3% in July, respectively, underpinned by rising real wages and softer financing conditions.

A contracting manufacturing sector in the Eurozone, with a PMI of 45.1 in November, and moderating services growth also weighed on the decision. The downward revision in growth, though, reflects mounting headwinds, including political instability in France and Germany, potential trade tensions with the United States, and persistent geopolitical tensions affecting energy markets.

"The risk of greater friction in global trade could weigh on euro area growth by dampening exports and weakening the global economy," Lagarde warned in December.

Despite mounting risks, some opportunities may still emerge.

Bright Spots Emerge Despite Challenges

Ireland leads growth projections with an expected GDP expansion of 4% in 2025 from -0.5% in 2024, driven by strong tech and pharmaceutical sectors. Poland is also expected to grow by 3.6 from 3%, followed by Greece at 2.3% from 2.1%.

With rate-sensitive sectors such as real estate and utilities expected to also benefit from monetary easing, Greece’s GEK Terna is well-positioned to profit from both public and private sector investments in real estate and infrastructure.

Greece is expected to see additional rewards from EU funding under the Recovery and Resilience Plan (RRR). The RRR prioritizes investments in infrastructure, real estate, and renewable energy, as well as a recovery in tourism, and urbanization and infrastructure development.

GEK Terna (GEKTERNA.AT) has significant investments in renewable energy, exposing it to Greece's booming investment environment under the RRP while aligning with EU funding priorities.

As public debt declines and macroeconomic conditions in 2025 are poised to improve, Terna’s forward dividend yield of 1.35% and ROE of 12.26% make it a top undervalued pick for 2025 and beyond. Analysts expect the stock to increase another 30% in the following year alone.